Chapter 9

Rental income and expenses

ey.com/EYTaxGuide

This chapter discusses rental income and expenses. It also covers the following topics.

- Personal use of dwelling unit (including vacation home).

- Depreciation.

- Limits on rental losses.

- How to report your rental income and expenses.

If you sell or otherwise dispose of your rental property, see Publication 544, Sales and Other Dispositions of Assets.

If you have a loss from damage to, or theft of, rental property, see Publication 547, Casualties, Disasters, and Thefts.

If you rent a condominium or a cooperative apartment, some special rules apply to you even though you receive the same tax treatment as other owners of rental property. See Publication 527, Residential Rental Property, for more information.

You may want to see:

527 Residential Rental Property

527 Residential Rental Property

534 Depreciating Property Placed in Service Before 1987

534 Depreciating Property Placed in Service Before 1987

535 Business Expenses

535 Business Expenses

925 Passive Activity and At-Risk Rules

925 Passive Activity and At-Risk Rules

946 How To Depreciate Property

946 How To Depreciate Property

4562 Depreciation and Amortization

4562 Depreciation and Amortization

6251 Alternative Minimum Tax—Individuals

6251 Alternative Minimum Tax—Individuals

8582 Passive Activity Loss Limitations

8582 Passive Activity Loss Limitations

Schedule E (Form 1040) Supplemental Income and Loss

Schedule E (Form 1040) Supplemental Income and Loss

In most cases, you must include in your gross income all amounts you receive as rent. Rental income is any payment you receive for the use or occupation of property. In addition to amounts you receive as normal rent payments, there are other amounts that may be rental income.

When to report. If you are a cash-basis taxpayer, you report rental income on your return for the year you actually or constructively receive it. You are a cash-basis taxpayer if you report income in the year you receive it, regardless of when it was earned. You constructively receive income when it is made available to you, for example, by being credited to your bank account.

For more information about when you constructively receive income, see Accounting Methods in chapter 1.

Advance rent. Advance rent is any amount you receive before the period that it covers. Include advance rent in your rental income in the year you receive it regardless of the period covered or the method of accounting you use.

Example. You sign a 10-year lease to rent your property. In the first year, you receive $5,000 for the first year’s rent and $5,000 as rent for the last year of the lease. You must include $10,000 in your income in the first year.

Canceling a lease. If your tenant pays you to cancel a lease, the amount you receive is rent. Include the payment in your income in the year you receive it regardless of your method of accounting.

Expenses paid by tenant. If your tenant pays any of your expenses, the payments are rental income. Because you must include this amount in income, you can deduct the expenses if they are deductible rental expenses. See Rental Expenses, later, for more information.

When a tenant pays to have capital improvements constructed on the landlord’s property and these improvements are not made in lieu of rent or other required payments, the value of these improvements is not income to the landlord, either when made or on termination of the lease, even though the landlord keeps the improvements at the end of the lease. However, the landlord will have no basis in the improvements and, therefore, cannot depreciate the improvements.

Susan rents an apartment to Pam. Pam, at her own expense, constructs a wall to separate the dining area from the living room. At the end of the lease, Pam vacates the apartment, leaving the wall. Susan does not record income at any time, even though she may benefit from the capital improvement. Susan may not depreciate the value of the wall because she has no basis in the wall.

If Susan must incur an expense to remove the wall and restore the property, it is either deducted from income or capitalized, depending on factors discussed later in this chapter.

Ken rents an apartment to Anthony for $550. Anthony pays for plumbing repairs of $150, which he in turn deducts out of his current month’s rent. Although Ken has received only $400 from Anthony, he must report the entire rent amount of $550 as income. Ken may also be able to report the $150 for plumbing repairs as a deductible expense.

Other examples of landlord expenses paid by a tenant that would be considered rental income include a tenant’s payment of a landlord’s real estate taxes, mortgage payments, or income taxes.

Property or services. If you receive property or services, instead of money, as rent, include the fair market value of the property or services in your rental income.

If the services are provided at an agreed upon or specified price, that price is the fair market value unless there is evidence to the contrary.

Security deposits. Do not include a security deposit in your income when you receive it if you plan to return it to your tenant at the end of the lease. But if you keep part or all of the security deposit during any year because your tenant does not live up to the terms of the lease, include the amount you keep in your income in that year.

If an amount called a security deposit is to be used as a final payment of rent, it is advance rent. Include it in your income when you receive it.

Part interest. If you own a part interest in rental property, you must report your part of the rental income from the property.

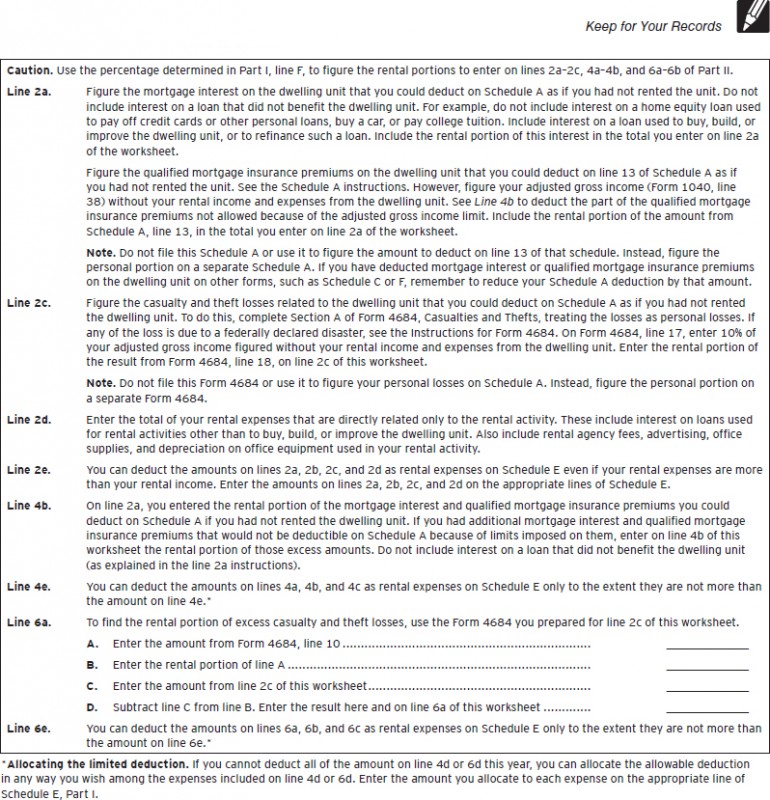

Rental of property also used as your home. If you rent property that you also use as your home and you rent it less than 15 days during the tax year, do not include the rent you receive in your income and do not deduct rental expenses. However, you can deduct on Schedule A (Form 1040) the interest, taxes, and casualty and theft losses that are allowed for nonrental property. See Personal Use of Dwelling Unit (Including Vacation Home), later.

This part discusses expenses of renting property that you ordinarily can deduct from your rental income. It includes information on the expenses you can deduct if you rent part of your property, or if you change your property to rental use. Depreciation, which you can also deduct from your rental income, is discussed later.

Personal use of rental property. If you sometimes use your rental property for personal purposes, you must divide your expenses between rental and personal use. Also, your rental expense deductions may be limited. See Personal Use of Dwelling Unit (Including Vacation Home), later.

Part interest. If you own a part interest in rental property, you can deduct expenses that you paid according to your percentage of ownership.

When to deduct. If you are a cash-basis taxpayer, you generally deduct your rental expenses in the year you pay them.

Depreciation. You can begin to depreciate rental property when it is ready and available for rent. See Placed-in-Service under When Does Depreciation Begin and End in chapter 2 of Publication 527.

Pre-rental expenses. You can deduct your ordinary and necessary expenses for managing, conserving, or maintaining rental property from the time you make it available for rent.

Uncollected rent. If you are a cash-basis taxpayer, do not deduct uncollected rent. Because you have not included it in your income, it is not deductible.

Vacant rental property. If you hold property for rental purposes, you may be able to deduct your ordinary and necessary expenses (including depreciation) for managing, conserving, or maintaining the property while the property is vacant. However, you cannot deduct any loss of rental income for the period the property is vacant.

Vacant while listed for sale. If you sell property you held for rental purposes, you can deduct the ordinary and necessary expenses for managing, conserving, or maintaining the property until it is sold. If the property is not held out and available for rent while listed for sale, the expenses are not deductible rental expenses.

Generally, an expense for repairing or maintaining your rental property may be deducted if you are not required to capitalize the expense.

Improvements. You must capitalize any expense you pay to improve your rental property. An expense is for an improvement if it results in a betterment to your property, restores your property, or adapts your property to a new or different use.

Betterments. Expenses that may result in a betterment to your property include expenses for fixing a pre-existing defect or condition, enlarging or expanding your property, or increasing the capacity, strength, or quality of your property.

Restoration. Expenses that may be for restoration include expenses for replacing a substantial structural part of your property, repairing damage to your property after you properly adjusted the basis of your property as a result of a casualty loss, or rebuilding your property to a like-new condition.

Adaptation. Expenses that may be for adaptation include expenses for altering your property to a use that is not consistent with the intended ordinary use of your property when you began renting the property.

The expenses you capitalize for improving your property can generally be depreciated as if the improvement were separate property.

Other expenses you can deduct from your rental income include advertising, cleaning and maintenance, utilities, fire and liability insurance, taxes, interest, commissions for the collection of rent, ordinary and necessary travel and transportation, and other expenses, discussed next.

Insurance premiums paid in advance. If you pay an insurance premium for more than one year in advance, for each year of coverage you can deduct the part of the premium payment that will apply to that year. You cannot deduct the total premium in the year you pay it.

Legal and other professional fees. You can deduct, as a rental expense, legal and other professional expenses, such as tax return preparation fees you paid to prepare Schedule E

(Form 1040), Part I. For example, on your 2014 Schedule E, you can deduct fees paid in 2014 to prepare your 2013 Schedule E, Part I. You can also deduct, as a rental expense, any expense (other than federal taxes and penalties) you paid to resolve a tax underpayment related to your rental activities.

Local benefit taxes. In most cases, you cannot deduct charges for local benefits that increase the value of your property, such as charges for putting in streets, sidewalks, or water and sewer systems. These charges are nondepreciable capital expenditures, and must be added to the basis of your property. However, you can deduct local benefit taxes that are for maintaining, repairing, or paying interest charges for the benefits.

Local transportation expenses. You may be able to deduct your ordinary and necessary local transportation expenses if you incur them to collect rental income or to manage, conserve, or maintain your rental property. However, transportation expenses incurred to travel between your home and a rental property generally constitute nondeductible commuting costs unless you use your home as your principal place of business. See Publication 587, Business Use of Your Home, for information on determining if your home office qualifies as a principal place of business.

Generally, if you use your personal car, pickup truck, or light van for rental activities, you can deduct the expenses using one of two methods: actual expenses or the standard mileage rate. For 2014, the standard mileage rate for business use is 56 cents per mile. For more information, see chapter 27.

Rental of equipment.

Only gold members can continue reading.

Log In or

Register to continue