Personal exemption amount increased for 2014. For tax years beginning in 2014, the personal exemption amount is increased to $3,950.

Standard deduction amount increased for 2014. The personal standard deduction amount for tax years beginning in 2014 is increased to $6,200 for unmarried taxpayers, $12,400 if married filing jointly or surviving spouse, $9,100 if head of household, and $6,200 if married filing separately.

Alternative Minimum Tax (AMT) exemption amount increased. For 2014, the exemption amounts for AMT are increased to $52,800 for unmarried taxpayers, $82,100 if married filing jointly or a surviving spouse, and $41,050 if married filing separately.

AMT exemption for a child with unearned income increased. The AMT exemption for a child whose unearned income is taxed at the parent’s rate has increased to $7,250.

Individual Shared Responsibility Payment.When you file your 2014 federal income tax return in 2015, you will report minimum essential health care coverage, report exemptions, or make any individual shared responsibility payment. If you don’t have coverage nor qualify for an exemption, you may have to make an individual shared responsibility payment when you file your 2014 income tax return. For 2014, generally, the payment amount is the greater of 1% of your household income above your filing threshold or $95 per adult ($47.50 per child) limited to a family maximum of $285. See Individual Shared Responsibility Provision—Calculating the Payment later in this chapter.

After you have figured your income and deductions as explained in Parts One through Five, your next step is to figure your tax. This chapter discusses:

The general steps you take to figure your tax,

An additional tax you may have to pay called the alternative minimum tax (AMT), and

The conditions you must meet if you want the IRS to figure your tax.

Your income tax is based on your taxable income. After you figure your income tax and AMT, if any, subtract your tax credits and add any other taxes you may owe. The result is your total tax. Compare your total tax with your total payments to determine whether you are entitled to a refund or if you must make a payment.

This section provides a general outline of how to figure your tax. You can find step-by-step directions in the Instructions for Forms 1040EZ, 1040A, and 1040. If you are unsure of which tax form you should file, see Which Form Should I Use? in chapter 1.

Tax. Most taxpayers use either the Tax Table or the Tax Computation Worksheet to figure their income tax. However, there are special methods if your income includes any of the following items.

Farming or fishing income. (See Schedule J (Form 1040), Income Averaging for Farmers and Fishermen.)

Unearned income over $2,000 for certain children. (See chapter 32.)

Parents’ election to report child’s interest and dividends. (See chapter 32.)

Foreign earned income exclusion or the housing exclusion. (See Form 2555, Foreign Earned Income, or Form 2555-EZ, Foreign Earned Income Exclusion, and the Foreign Earned Income Tax Worksheet in the Form 1040 instructions.)

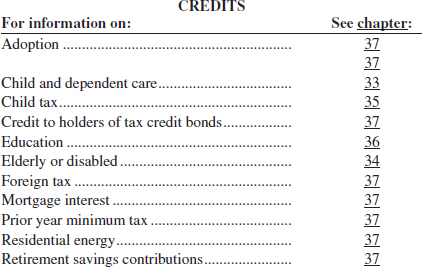

Credits. After you figure your income tax and any AMT (discussed later), determine if you are eligible for any tax credits. Eligibility information for these tax credits is discussed in chapters 33 through 37 and your form instructions. The following table lists the credits you may be able to subtract from your tax and shows where you can find more information on each credit.

Some credits (such as the earned income credit) are not listed because they are treated as payments. See Payments, later.

There are other credits that are not discussed in this publication. These include the following credits.

General business credit, which is made up of several separate business-related credits. These generally are reported on Form 3800, General Business Credit, and are discussed in chapter 4 of Publication 334, Tax Guide for Small Business.

Renewable electricity, refined coal, and Indian coal production credit for electricity and refined coal produced at facilities placed in service after October 22, 2004 (after October 2, 2008, for electricity produced from marine and hydrokinetic renewables), and Indian coal produced at facilities placed in service after August 8, 2005. See Form 8835, Part II.

Text intentionally omitted.

Credit for employer social security and Medicare taxes paid on certain employee tips. See Form 8846.

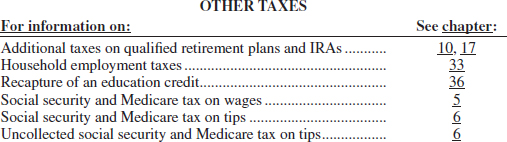

Other taxes. After you subtract your tax credits, determine whether there are any other taxes you must pay. This chapter does not explain these other taxes. You can find that information in other chapters of this publication and your form instructions. See the following table for other taxes you may need to add to your income tax.

You also may have to pay AMT (discussed later in this chapter).

There are other taxes that are not discussed in this publication. These include the following items.

Self-employment tax. You must figure this tax if either of the following applies to you (or your spouse if you file a joint return).

Your net earnings from self-employment from other than church employee income were $400 or more. The term “net earnings from self-employment” may include certain non-employee compensation and other amounts reported to you on Form 1099-MISC, Miscellaneous Income. If you received a Form 1099-MISC, see the Instructions for Recipient on the back. Also see the Instructions for Schedule SE (Form 1040), Self-Employment Tax; and Publication 334, Tax Guide for Small Business.

You had church employee income of $108.28 or more. Text intentionally omitted.

Recapture taxes. You may have to pay these taxes if you previously claimed an investment credit, a low-income housing credit, a new markets credit, a qualified plug-in electric drive motor vehicle credit, an alternative motor vehicle credit, a credit for employer-provided child care facilities, an Indian employment credit, or other credits listed in the instructions for Form 1040, line 62. For more information, see the instructions for Form 1040, line 62.

Section 72(m)(5) excess benefits tax. If you are (or were) a 5% owner of a business and you received a distribution that exceeds the benefits provided for you under the qualified pension or annuity plan formula, you may have to pay this additional tax. See Tax on Excess Benefits in chapter 4 of Publication 560, Retirement Plans for Small Business.

Uncollected social security and Medicare tax on group-term life insurance. If your former employer provides you with more than $50,000 of group-term life insurance coverage, you must pay the employee part of social security and Medicare taxes on those premiums. The amount should be shown in box 12 of your Form W-2 with codes M and N.

Tax on golden parachute payments. This tax applies if you received an “excess parachute payment” (EPP) due to a change in a corporation’s ownership or control. The amount should be shown in box 12 of your Form W-2 with code K. See the instructions for Form 1040, line 60.

Tax on accumulation distribution of trusts. This applies if you are the beneficiary of a trust that accumulated its income instead of distributing it currently. See Form 4970 and its instructions.

Additional tax on HSAs or MSAs. If amounts contributed to, or distributed from, your health savings account or medical savings account do not meet the rules for these accounts, you may have to pay additional taxes. See Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans; Form 8853, Archer MSAs and Long-Term Care Insurance Contracts; Form 8889, Health Savings Accounts (HSAs); and Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts.

Additional tax on Coverdell ESAs. This applies if amounts contributed to, or distributed from, your Coverdell ESA do not meet the rules for these accounts. See Publication 970, Tax Benefits for Education, and Form 5329.

Additional tax on qualified tuition programs. This applies to amounts distributed from qualified tuition programs that do not meet the rules for these accounts. See Publication 970 and Form 5329.

Excise tax on insider stock compensation from an expatriated corporation. You may owe a 15% excise tax on the value of nonstatutory stock options and certain other stock-based compensation held by you or a member of your family from an expatriated corporation or its expanded affiliated group in which you were an officer, director, or more-than-10% owner. For more information, see the instructions for Form 1040, line 62.

Additional tax on income you received from a nonqualified deferred compensation plan that fails to meet certain requirements. This income should be shown in Form W-2, box 12, with code Z, or in Form 1099-MISC, box 15b. For more information, see the instructions for Form 1040, line 62.

Interest on the tax due on installment income from the sale of certain residential lots and timeshares. For more information, see the instructions for Form 1040, line 62.

Interest on the deferred tax on gain from certain installment sales with a sales price over $150,000. For more information, see the instructions for Form 1040, line 62 and Publication 537, Installment Sales.

Excess advance premium tax credit repayment.For more information, see the instructions for Form 8962.

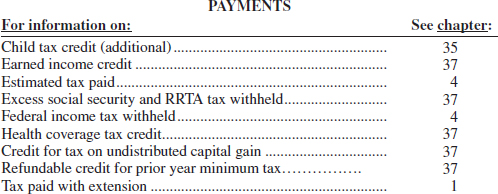

Payments. After you determine your total tax, figure the total payments you have already made for the year. Include credits that are treated as payments. This chapter does not explain these payments and credits. You can find that information in other chapters of this publication and your form instructions. See the following table for amounts you can include in your total payments.

Another credit that is treated as a payment is the credit for federal excise tax paid on fuels. This credit is for persons who have a nontaxable use of certain fuels, such as diesel fuel and kerosene. It is claimed on Form 1040, line 72. See Form 4136, Credit for Federal Tax Paid on Fuels.

Refund or balance due. To determine whether you are entitled to a refund or whether you must make a payment, compare your total payments with your total tax. If you are entitled to a refund, see your form instructions for information on having it directly deposited into one or more of your accounts, or to purchase U.S. savings bonds instead of receiving a paper check.

This section briefly discusses an additional tax you may have to pay.

The tax law gives special treatment to some kinds of income and allows special deductions and credits for some kinds of expenses. Taxpayers who benefit from this special treatment may have to pay at least a minimum amount of tax through an additional tax called AMT.

Only gold members can continue reading. Log In or Register to continue