Framing a Canvas for Shipping Strategy

Chapter 29

Framing a Canvas for Shipping Strategy

Kurt J. Vermeulen*

1. Introduction

A voluminous body of research and literature has been produced in the domain of strategy for non-shipping companies. Yet, the shipping industry which transports more than 90% in volume of those companies’ physical output has been allotted an altogether humble share of strategy researchers’ time. It is only in the 1970s and 1980s that we see strategy literature coming to the fore, perhaps not coincidentally in periods when shipping experiences its periodical crises. Recently, strategy for ocean shipping companies has enjoyed somewhat more of an interest from various angles including economic historiography, organisational behaviour, operational research, game theory, behavioural economics and quantitative finance. In the public’s mind, shipping is readily associated with some of its charismatic denizens past and present like Aristoteles Onassis, Stavros Niarchos, Erling Naess, John Fredriksen and Chang Yung-fa. This is testimony to the entrepreneurial nature of the shipping industry, and entrepreneurs tend by nature, and out of business necessity, to take a holistic view. It is this wider, more holistic, approach which deserves more attention in future research. Prior to engaging in such a review, it is necessary to assess where shipping strategy stands in the literature to date and how holistic in nature this strategy analysis has been.

Section 2 sets out the approach this author adopted in finding and selecting the literature to review and analyse. Out of this analysis came a distinct three pronged approach consisting of: (i) a review and analysis of the strategy literature “proper”; (ii) the development of a conceptual framework for literature classification taking into account the holistic and entrepreneurial nature of a shipping entrepreneur’s perspective; and (iii) a review and analysis of the literature with reference to the proposed conceptual framework. The section proceeds in outlining the proposed conceptual framework. Section 3 adopts this approach and makes a start with a review and analysis of the strategy literature “proper”. It, firstly, gives a brief overview of key authors who have influenced the theory of strategy applied to shipping and, then, focuses in particular on Michael Porter’s work whose strategy theory and concept of sustainable competitive advantage have come to dominate the field of shipping strategy. Section 4 discusses the strategy literature pertaining to shipping specifically. Section 5 draws some conclusions from this analysis, whilst Section 6 will complete the review by outlining broader areas for future research.

2. Data and Methodology

With a view to gather the largest possible body of literature on the subject matter, we performed an English language only database search on EBSCO Business Source and EconLit covering their full historical extent. The search string terms encompassed simply shipping, maritime and strategy keywords. This generated some 120,000 headlines which were summarily reviewed. Some 800 articles, all shipping specific, published between 1965 and March 2010 were retained for further screening. Of those, we retained for incorporation in this review nearly 100 articles published in peer reviewed academic journals. The remainder of articles is in use for the suggested future research. Further, our literature review also encompasses material taken from various monographs or edited collective volumes. The author does not profess this and subsequent reviews to be exhaustive, but does believe it to be sufficiently encompassing to get a good understanding of the state of research in the ocean shipping strategy domain.

Having reviewed this literature, we found a very broad range of topics being addressed from a topical or discipline perspective, yet whose relevance to strategy does not seem to be explored further. Many journal contributions from a maritime economics perspective explore in a robust manner issues such as the value of time and flexibility, yet find little echo in the strategy literature with respect to the impact of the need for, and value of, flexibility. Or, still, corporate finance instruments such as the use of financial derivatives may be explored in great detail with respect to hedging efficiency yet find their relevance for paper based shipping activities, asset portfolio composition and risk management policies quasi ignored from a shipping strategy perspective. This author thinks this may be partly due to the specialist nature many of the social scientists have been led to adopt over time. Gone seem the times when Stanley Sturmey (1962) would report on the state of British shipping and review the whole field of maritime economics in the process, or Moreby (1975) would review the role of the human element in shipping and place such in a technoeconomic context whilst having also regard for relevant findings in the fields of psychology and organisational behaviour. But, have those times really gone? Stopford’s (2009) authoritative work has grown from a maritime economics textbook (Stopford, 1988) into a veritable compendium of the economic history of the shipping industry and research pertaining to it. Wijnolst and Wergeland (2009) are in the process of doing the same in the field of shipping technology and innovation by bringing together various strands of research ranging from strategy to ship design to innovation theory. These are signs that the call for a return of “Renaissance Man” is being echoed in the field of maritime economics in particular and the study of shipping in general.

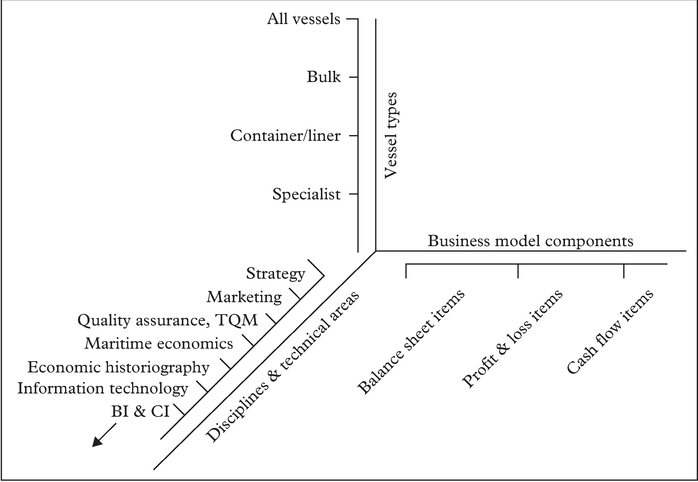

This author’s attempt to contribute to this recent development is to seek to place the substantial extant body of literature in a more holistic framework reflecting the reality that shipping strategy pertains not just to the group level strategic objectives, but also to its implementation in specific market segments or its implementation through various operational and managerial functions. As such, it is proposed to classify the literature

Source: Author

by means of a three-dimensional grid representing a holistic entrepreneurial approach (see Figure 1 above). It has as advantage that we cover not only the pure strategy literature, but also the non-strategy literature whose findings are of relevance to strategy or the very application of it.

The first dimension represents the key financial statements of any business enterprise; a balance sheet, profit and loss statement (P&L) and a cash flow statement. In this manner, any aspect of the strategy literature should be related back to any of the business attributes affecting a company’s financial performance, but also vice versa. That is, one assesses the implications for strategy of the literature pertaining to topical non-strategy matters. Those financial statements can also be subdivided into their component business attributes. The subdivision this author proposes is for conceptual purposes and not necessarily compliant with accounting rules, such as IFRS. For examples we and the management science literature may treat a management team as a company’s intangible asset albeit this would not meet IFRS classification requirements. The balance sheet encompasses assets, liabilities and Ordinary Shareholders’ Funds (OSF). Assets in the shipping business would comprise tangible assets (e.g. vessels, offices, handling terminals) and intangible assets (e.g. brand name, know how, customer list, the team of key employees, software, patents, trademarks, design rights, database rights, trade secrets, rights under concession agreements and rights to berthing slots or container slots). The liabilities consist of debt whilst the OSF encompasses equity, reserves and minority interests.

The P&L components used in our proposed classification are not those commonly found in the eponymous financial statement, but three of the five key models constituting jointly a business model (Mullins and Komisar, 2009). They are the revenue model, the gross margin model and the operating model. The two other models are the working capital model and the investment model, both of which fall under the cash flow component of this dimension of our classification. The revenue model pertains to questions such as: whom to sell to, what to sell, why does the customer buy this, when do they buy it, what services to provide as part of the sale and at what price? The gross margin model addresses the cost of sales such as brokerage fees payable to ship brokers, costs of goods sold (COGS) encompassing bunkers and labour, port fees, survey fees and, crucially, the choice of margin mix (time charter/COA/FFA vs. spot market, portfolio composition). The operating model (OPEX) addresses sales, general and administrative expenses (S,G&A) including ship management fees, freight rates payable, hedging costs and, importantly, those costs associated with the provision of non-standard specific services requested by the customer. Finally, the working capital model addresses the working capital components that influence timing of cash flows such as inventory (e.g. capacity), debtors (e.g. freight receivable) and creditors (e.g. supplier invoices owed) whilst the investment model addresses capital expenditure (CAPEX) on either new assets or Research and Development (R&D).

The second dimension of our proposed classification grid is composed of the shipping market as a whole, and could be considered as part of future research to be expanded to include specific shipping market segments, respectively bulk (dry bulk, liquid bulk, break bulk and neo-bulk), liner/container and specialty (e.g. chemicals). A third, and final, dimension of our proposed grid consists in effect of the various disciplines or technical areas whose practitioners have made contributions that are pertinent to strategic planning in the ocean shipping industry including in no particular order, law (competition law, antitrust law), organisational behaviour, behavioural economics, marketing, economic geography, scenario planning, governance, business intelligence, competitive intelligence, corporate social responsibility, information technology, operational research, logistics/supply chain management, quality assurance/total quality management and economic historiography and, of course, strategy. It is this variety of disciplines whose contributions are to be reflected in future research, which will most aptly illustrate the holistic nature of strategy.

In this contribution, we will now focus on the literature of strategy proper pertaining to the ocean shipping industry in general (i.e. to the exclusion of a review of strategy literature specific to a single shipping market segment).

3. About Strategy Proper and Shipping

3.1 What is strategy?

It is only fitting that we start our review with the literature pertaining to strategy proper. Strategic choices made by shipping companies will address the Where and How to compete and, therefore, consist of corporate strategy and business strategy (Grant, 2008). Corporate strategy addresses the markets within which a shipping firm decides to compete (e.g. dry bulk, chemicals, CPP, oil) and will address decisions on vertical integration, diversification, horizontal integration, new ventures, divestments and allocation of resources between the different businesses. The business strategy, aka competitive strategy, addresses how the shipping firm will establish a competitive advantage over its rivals. Finally, strategy gets implemented on the functional level or business line level. Strategy can fulfil a variety of functions in the firm, e.g. communication across organisational units, decision support, facilitating organisational learning and, most importantly, set targets. Strategy is not a product, but a continuous process making use of strategy tools (e.g. industry analysis) in researching, devising, implementing strategy and controlling its execution.

3.2 The evolution of the theory of strategy

Before proceeding with a review of shipping strategy literature, it is perhaps appropriate to outline the evolution of the theory of strategy, as summarised by Michel Godet (Godet, 2007). Godet considers Henri Fayol (Fayol, 1916) as one of the founding fathers of “planning”. Fayol summarises management as anticipation, organisation, command, coordination and control. His contribution was to translate management into 14 principles including but not limited to, the division of labour, unity of command, the subordination of specific interest to the general interest, centralisation and decentralisation, unity of direction, remuneration, stable work force, initiative, solidarity with personnel, equity and order. It is notable that several of these ideas are only now coming back to the fore.

Contrary to Fayol’s ideas and the then prevailing Fordism, Mary Parker Follett (1924) pioneered the behaviourist approach to management built on decentralisation, the role of the group as an integrating entity for individuals, competency-based authority and control through trust and communication. The Interbellum was characterised by the separation of strategic from tactical plans and the diffusion of statistical and financial techniques, a by-product of war time logistics planning by means of operational research. Note, in this respect, the genesis of modern day econometrics by Tjalling Koopmans, and its pioneering application to tanker freight rate forecasting and tanker shipping cycle analysis (Koopmans, 1939). DuPont de Nemours and General Motors, then under the chairmanship of Alfred P. Sloan, started applying those new principles to their respective organisations, which were characterised by divisional objectives setting. A Sloan contemporary contributed to the reorganisation of GM and subsequently wrote the “Concept of the Corporation” (Drucker, 1946) about the newly formed multi-divisional company.

Drucker (1955) then went on to posit the five fundamental activities of a manager: setting objectives, structuring the firm and organising personnel, motivating, communicating, setting performance targets, supervising and developing staff. The 1950s and 1960s feature the nascent discipline of long-range planning which adds a long term planning component to the annual budgeting cycle. This rapidly became corporate planning as the needs for corporate wide growth targets and diversification policies were acknowledged. Chandler (1962) observed the organisational setup changed only through trial and error in reaction to environmental changes. Ansoff (1965) argued for a proactive approach through reorganisation of the corporation based on the anticipation of environmental change. The feelings of insecurity engendered by the recession of 1973 reinforced the need for corporate planning, now strategic planning, taking into account the possible futures. Ansoff (1979) argued against the redundant character of planning based on a priori objectives and advocated strategic management (i.e. the capability to react and adapt to environmental change). Porter (1998b) developed approaches to competitive analyses of firms and industries around the concept of sustainable competitive advantage. Barney (1991) reoriented the concept of sustainable competitive advantage towards the unique internal resources of the firm, thus, creating a resource-based theory of the firm (Conner, 1991). The concepts posited by Porter, and more recently Barney, are the ones that have come to dominate the shipping strategy literature.

3.3 The market structure and features of ocean shipping

Strategy is a function of the market features in which the subject company is active. The demand for shipping services, as a transport function, is a derived demand correlated to the general economic development. Developments in shipping, such as technological innovation, and associated freight rate declines based on resultant economies of scale, cannot by themselves lead to enlargement of the demand for shipping services. Jacks and Pendakur’s (2008) analysis of the 1870–1913 globalisation movement showed income growth and convergence were the drivers of world economy globalisation, and not the maritime transport revolutions of steamships, metal hulls and propellers. Maritime innovation and its corollaries are the result of a “demand” for economic growth.

The market structure of shipping is, firstly, characterised by serving mainly industrial consumers with an ocean going merchant fleet comprising 26,280 vessels owned by 4,795 companies (Stopford, 2004). In other words, the average shipowner has five vessels and is, thus, unlikely to be able to exercise influence over the market.

The market’s main transactional currency was the US Dollar, albeit anecdotal evidence suggests this may be under review after the 2007/2008 credit crunch led to a severe decline in the dollar value. Vessels are high capital investment assets and have an economic lifetime of over 20 years. Earnings are highly volatile as the demand for shipping services is a derived demand linked to the world business cycle.

Bulk markets are very competitive, which competitiveness is aided by homogenous cargo, many market participants (both ship operators and shippers), low barriers to entry besides capital investment and adequate information flows ensuring market transparency. Specialist shipping markets have fewer customers and fewer market participants and competition is focussed on service and specialisation. There can be substitution between some vessels operating in specialised market segments and those operating in the bulk segments (e.g. combined vessels). Liner shipping serves both volume shippers directly (e.g. full truck load with truck meaning a TEU container) as well as lessthan-truckload [LTL] shippers through freight forwarders or Non Vessel Operating Common Carriers [NVOCCs]. Stopford (2004) considers liner competition mostly from a price perspective. Finally, in all market segments, shipping operators engage in various forms of collaboration including shipping pools with a view to improve service frequency, asset utilisation and transport efficiency. Fearnley Consultants (Fearnleys, 2007) estimated approximately 40 pools were in operation as of 2007, whereby the pool operator operates in nearly all cases independently from the pool members.

Further, there is an established view that going long, by entering into longer term chartering arrangements (COAs, FFAs, Time Charters) is a risk averse strategy whilst going short, i.e. trading spot, is more risky (Lorange and Norman, 1973). The recent shipping boom has shown, though, that going long may have its own risks, such as charter default risk. Charter default risk is, finally, one risk aspect of the shipping business in addition to business risk, liquidity risk, default risk, financial risk, non-charter credit/counterparty risk, market risk, political risk, technical risk and physical risk (Kavussanos and Visvikis, 2006). Any strategic plan should address how all such risks will be managed and compensated for through an appropriate return.

4. Strategy Literature Pertaining to Shipping Overall

This section reviews the strategy literature in relation to the ocean shipping industry as a whole (i.e. addressing shipping as a single market, rather than specific shipping market segments).

4.1 The drivers of formal strategies and strategy processes

4.1.1 Internal drivers

Throughout countries, shipowners have operated for many years in a “club system” whereby the long-time practice of shipping, sometimes across many family generations, engendered trust between rival ship owners enabling cooperation. This is not new in itself, as shown by the history of Greek or Spanish shipping in late nineteenth century (Valdaliso, 2000; Theotokas and Harlaftis, 2009). The use of conferences and shared ownership and promotion of an idiosyncratic business culture would further the build-up of such confidence between parties even if they had never worked together before – the club membership vouchsafed for a common set of values (Miller, 2003). An increase in demand for maritime transport and technology-led operational improvements led to a heavy rise in capital requirements which were, initially, met by horizontal integration on the back of established social networks built around trust and loyalty. This club approach minimised transaction costs. It is only during a later stage shipowners sought vertical integration albeit with risk mitigation through transactions involving only other shipping related activities such as shipbroking and stevedoring, as Valdaliso (2000) illustrates with the evolution of Spanish shipping.

However, we can surmise that the club approach was no longer sufficient as the changing economic environment for shipping led to an increasing capital intensity of shipping and a concurrent rise in the concentration of tonnage supply. Whilst this concentration might to “a considerable extent” be indigenous, citing liner consortia as an example (Metaxas, 1978), its resulting requirement was for massive capital injections which were unlikely to have been met from within the “club”. The time had come for seeking funds externally and plan for a business with more risk factors than before. This did not imply that shipping lost its human touch, as business development would remain for a long time dependent on the social networks built through the eponymous “business trip” (Miller, 2003).

The increasing internationalisation of shipping with respect to capital raising and market participants, the rise of offshore flag of convenience registries and shipping joint ventures between developing countries and the developed world also implied that shipowners were now exposed to a far wider range of risk factors whose assessment required a more structured approach (Metaxas, 1978; Frankel, 1982b). The increasing vessel sizes and technological complexity also led to more complex management (Frankel, 1982a).

Greek shipping, though, resisted the implications of those trends for a long time under influence of its fragmented ownership, familial character and idiosyncratic business philosophy (Theotokas and Harlaftis, 2009). For Greek shipowners, shipping was not so much a cash flow generating business as a lifestyle, an “arena”. Professional managers were only hired in those businesses which had various non-shipping activities or had reached such a scale as to require non-familial assistance. In Greece, the outsourcing of ship management to third parties can be a reflection of disagreements among family members and the need to see those resolved by having independent third parties brought in (Mitroussi, 2004). It is those parties, in turn, who will insist on a strategic plan meeting with their approval.

A final consideration pertaining to the internationalisation of shipping is the oft quoted life cycle theory of industries by Vernon (1966). The starting point of all industrial innovation is that pioneering business ideas are first executed in those markets where the entrepreneur, for it is the entrepreneur who pioneers, is privy to the most effective communication between the potential market (demand) and the potential supplier (supply). It is not the factor inputs and their cost which are important in an Early Stage market, for price elasticity is low, but the market feedback allowing for proper product specification and externalities. The product is unstandardised so that the producer can change inputs at leisure, and as a result production is not cost but specification driven based on effective market feedback. The Maturing Product exhibits a certain degree of standardisation to allow for production economies of scale (reduced labour cost, increasing capital cost), albeit some differentiation is retained as a competitive advantage with which to avoid price competition. The market has by now accepted a set of general standards and probability of demand is being complemented by increasing certainty of cost estimates and increasing price elasticity. Exports and production relocation are considered where labour cost advantages in target markets are lower than domestic labour and freight costs combined or, more importantly, where a strategic threat to future exports emerges. The Standardised Product is now highly standardised and has well established export markets whilst retaining further export potential. The price elasticity is very high and production processes are now “set” so as to allow for high capital investment in machinery allowing for maximum economies of scale (low labour input, high capital input). Competition is now fought on the basis of innovation induced by direct market feedback (information). Imports into the market are characterised by high labour input and vertical integration into “external economies” (i.e. capital inputs which are not readily available in the exporters’ markets and thus need to be secured). Thus, the original export market will by now invest in low risk self-contained production processes for standardised products with little inventory risk.

The life cycle theory has been applied by some authors to shipping (Sletmo, 1989; Tenold, 2009; Thanopoulou, 1995). It has the merit to provide a simple canvas on which to draw a shipping strategy and suggests in essence that any industry will have to continuously reinvent itself as a pioneer if it does not wish to be superseded by competitors emanating from erstwhile export markets. This emphasises the need for any shipowner to possess at all times a clear strategic plan as to how to continue to innovate on the basis of ever more skilled labour inputs and differentiated service offerings so as not to wither away as a mature industry.

4.1.2 External drivers

The need for external funds, (i.e. funds from outside the traditional shipping community) required a vetting of the corporate strategy and shipping marketing approaches by third party financiers (Goss, 1987; Grammenos, 1979; Syriopoulos, 2007; Grammenos and Choi, 1999). This is especially so as the capital requirements are several magnitudes of the annual cash flow their investment may generate. It is ironic, then, that the availability of finance is also held responsible for the homogenisation of strategy in that easy credit has pushed investors to fund more and more “niche” operators turning the niche market into a “commoditised” shipping market (Lorange, 2005).

Regardless, it is one thing to have a strategy and quite another to successfully communicate such to third parties. Shipping companies have many difficulties in accessing the bond markets on competitive terms as a consequence of failing to obtain favourable ratings from the rating agencies. The latter is in turn being attributed to shipping companies’ failure in getting rating analysts sufficiently comfortable with the esoteric specificities of the shipping industry (Leggate, 2000). Thus, the strategy process should also address the ability of the shipping company to adequately communicate its adopted strategy to third parties with a view to obtain, inter alia, a lower cost of funding and better access to external funding.

In addition, shipping has become an increasingly regulated industry with its objectives coming under scrutiny of regulatory authorities. The increasing public involvement in service industries and the increase in complexity of shipping require shipping companies to frequently revisit their stated objectives (Frankel, 1982b).

4.2 Setting a strategic objective for shipping companies

Whilst some companies operate with their strategy emerging as they go along, others set a strategic objective and set out to achieve this through the strategy process. The wording of such an objective is critical as it needs to embody the current and future activities of the shipping company. Flexible objectives are, thus, argued for (Rich, 1978b). For example, state as objective the “provision of transport” rather than the provision of mere “ocean shipping”. Frankel (1982a) considers too little attention is being paid to formulating objectives and, if any, to setting criteria of the shipping enterprise. Criteria such as profit maximisation, utilisation maximisation, market share maximisation can be internally conflicting and need proper drafting to facilitate planning implementation. To obtain flexibility, an effective feedback process needs to be devised so as to ensure the periodic or even continuous assessment, and if required, restatement of the strategic objectives of the shipping company (Frankel, 1982b).

To be motivational and permit a long-term perspective, the objectives should also target growth (Rich, 1978b). Whilst objectives should be internally consistent (i.e. not in conflict with one another) they should also be consistent with existing resource commitments, fit the company’s capabilities and requirements, such as prior or traditional commitments (Frankel, 1982b). Also, prior to formulating its objective(s), the organisation should have assessed its strengths and weaknesses by means of a review of past and present performance and failures (Langley Jr, 1983). Langley also suggests a mission statement as a prerequisite to formulating strategic objectives. Note the absence in the shipping strategy literature of the concept of shipping companies having to articulate a “vision”.

4.3 Process and organisational features of strategy development

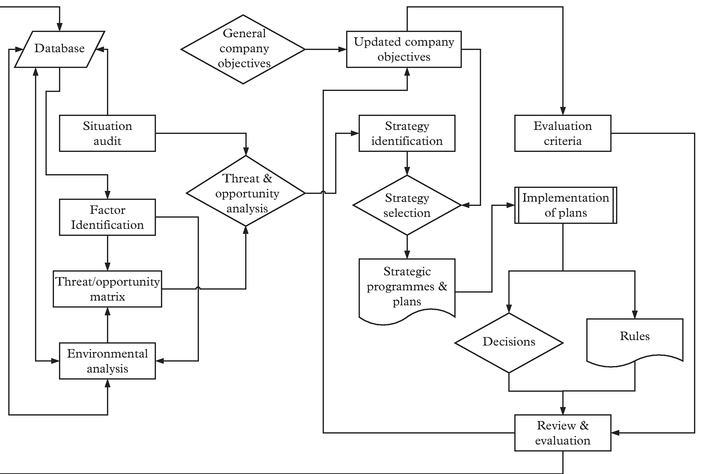

The earlier literature (Rich, 1978a; Frankel, 1982b) on shipping strategy analysed the corporate planning process in selected shipping companies and placed their strategies

Source: Adapted from Frankel (1982b)

in the context of the frameworks developed by strategy authors, such as Drucker and Ansoff.

A graphical overview of a strategy process is shown in Figure 2 above.

4.3.1 Planning approaches

Two planning approaches are distinguished; a “top down” or hierarchical approach and the decentralised “bottom-up” approach. This establishes also the link between planning and organisational structure, the latter being a tool to enable the former. Frankel (1982a) distinguishes between two poles of organisation, the traditional centralised hierarchical structure and the organismic decentralised structure. The former is a hierarchy of command, control and communication paired to top level concentration of information. The latter is a network with distributed knowledge and those centres of knowledge become, on a topical basis, centres of control. A shipping company will use the former if dealing with a known slowly changing environment, and the latter when operating in changing conditions. In reality, acknowledges Frankel, a shipping company will opt for a mix of both management systems and approaches which can result in adoption of a matrix structure.

Notwithstanding, Frankel (1982b) is decisively in favour of the top down approach and argues the responsibility for planning lies with the elected Board of Directors regardless of the organisational setup (Frankel, 1982a). Note that Frankel uses terms such as policy and planning, with the former seemingly referring to strategic planning and the latter more to competitive planning and functional planning (infra). An alternative view of those respective approaches is to label them as portfolio approach (topdown) and deal view (bottom-up), as Lorange (2001) does. Put another way, the top down approach can address the shipping company’s activities from a portfolio level, whereas the bottom-up approach addresses the vessels (aka bottoms). Note in this respect that both Lorange (2001) and Stopford (2004) consider every single vessel as a business unit in its own right.

Hawkins and Gray (2000) developed a taxonomy of non-shipping specific strategies tailored for application to different organisational levels (i.e. the traditional distinction between corporate planning (at group level), competitive or business planning (at business unit level) and functional planning (at business line level)). However, the predominance of smaller shipping companies with a fleet size not exceeding five vessels suggests a flat organisation with single level planning activities, if at all. The planning process participants’ hierarchical position may also provide some indications in this respect. Notwithstanding, planning at various organisational levels may occur within the minority of bigger shipping groups (e.g. liner shipping conglomerates).

In arguing for a top-down approach, Frankel reflects the established planning practice of Greek shipping where CEO involvement extends to setting aims and objectives, choosing alternatives, controlling and evaluating the company’s operations (Koufopoulos et al., 2005). Involvement of the CEO has a signalling function with respect to the importance of the process (Frankel, 1982b). The advantage of the top down approach is that it may also address venturing into new business areas which a bottom-up approach is less likely to contemplate due to a self-preservation instinct among divisional heads. This is in contrast to Rich (1978b) who argues hierarchical top-down planning processes are assessed as more risk averse, as reflected in the incremental nature of their strategy initiatives, whereas bottom-up approaches tend to be more entrepreneurial and risk-friendly. Lorange (2001) argues a balance should be struck between both approaches by adopting a complementary process.

The risk friendliness of the shipping company in choosing a strategy is argued by Rich (1978b) to be linked to the prevailing planning approach. The organisational structure is reactive to environmental changes and the strategic objectives are consequently affected by the interplay between ownership and management control. The hierarchical approach will typically be driven by a central planning staff (Rich, 1978a). The observed lack of participation of lower- and middle-management levels, as opposed to the key role played by the CEO, in Greek (Koufopoulos et al., 2005) and Asian-Pacific (Hawkins and Gray, 1999) shipping companies’ planning processes confirms this approach. However, planning approach should not be confused with the extent of participation of staff at all hierarchical levels in the planning process.

4.3.2 Planning process elements

A textbook strategy process proper, an illustration of which was shown in Figure 2 above, commences with an assessment of internal and external factors with strategic influence. In the process drawn by Frankel (1982b) this is termed factor identification. Various methodologies exists which are non-shipping specific and, hence, need not be elaborated on in this review. Notwithstanding, it is appropriate to briefly mention the relevance of competitive intelligence in this respect.

4.3.2.1 Competitive intelligence

Aristoteles Onassis was well known to carry around with him at all times a notebook in which he duly noted anything or everything that was relevant to his business. Onassis intuitively practiced a form of competitive intelligence (CI) gathering. In industries other than shipping, this intuitive CI gathering has been formalised and institutionalised and has become the preserve of competent professionals. In those organisations, competitive intelligence is a systematic programme for gathering and analysing information about your competitors’ activities and general business trends to further one’s own company’s goal (Kahaner, 1997). CI should not be confused with business intelligence (BI), which pertains to internally generated and thus company specific data devoid per se of relevance to the competitive environment. BI is, however, useful in benchmarking exercises whereby the shipping company can measure its strengths and weaknesses in operational and financial performance against those of its competitors.

To perform an assessment of internal and external factors with strategic relevance to the firm, CI gathering and analytical processes are the tools of the trade. It is notable that Asia-Pacific shipping companies’ strategy processes tend to attribute more importance to informal discussions between experienced executives exchanging, in effect, internalised CI rather than practising formalised strategy development processes (Hawkins and Gray, 1999). By way of illustration, Evergreen’s founder stated the management philosophy of his company is, inter alia, to stay well informed to ensure a company’s sustained competitiveness. Evergreen’s employees are the backbone of the company’s long-term survival, suggesting in the process employees always need to keep their eyes and ears open for CI (Chang, 1999). It can be surmised the CI gathering and analysis process is well formalised in Evergreen. Onassis and Evergreen are therefore good illustrations of two of the three stages of competitive development as described by West (2001). Onassis was competitor aware, his data collection was informal in nature and based on a natural curiosity albeit without a reported organisational setup or systems backup for managing his CI. Evergreen is probably competitor intelligent with a formal data collection process, for application in anticipating competitor moves and industry trends, managed by a CI manager who enjoys the backup of dedicated IT-based CI systems. In between these two states is the competitor sensitive company, which combines both informal and formal approaches to gather CI on competitors with a view to emulate them. This responsibility often lies with the marketing management information officer who uses for this purpose an existing marketing information system. An example of the latter approach was documented for erstwhile chemical shipping company Panocean-Anco (Tomlinson, 1980).

Shipping is generally considered to be a secretive industry whilst the wide availability of data sources is only a recent phenomenon. Yet, shipping pioneered the gathering and use of competitive intelligence with the use of “cartographers” like Ortelius and Mercator. Or, the East India Company sending Hakluyt in 1602 to report in 500 volumes on navigation, geography, resources, politics and economics (Moeller and Brady, 2007). Zannetos is reported in Ronen (1980) to have said that the reason behind secrecy in shipping is the inability of those who possess the data to use it for managerial decisions. Ronen puts this comment in a context of a multitude of data sources (data overload), lack of data selectivity (lack of information), lack of comparisons and summaries (no topical analytical capabilities). This is a frequent problem with competitive intelligence gathering, or rather explaining the lack thereof. Ronen’s (1981) case study reports on a successful implementation of a commercial intelligence system in shipping companies to gather competitive intelligence which in turn can be used in a strategy setting process including trade flow estimation, freight rate determination and competitor analysis.

There is, thus, some evidence that shipping companies have moved on from Onassis’ CI practice towards becoming more competitor sensitive. This is particularly relevant as shipping strategies are often considered to be imitative, as illustrated by Greek shipping (Theotokas and Harlaftis, 2009). However, it is noteworthy that some organisations have elevated CI gathering to formalised processes practiced by all employees with a view to maximise the intelligence gathered. This is in contrast to the documented practice (see below) of keeping strategy confined to top management with little to no participation by middle management and lower-level executives. This puts into question to what extent the resulting strategies are reflective of the evolving competitive environment as experienced first hand by those latter executives.

Once the internal and external data have been gathered, they will need to be categorised and structured in a framework after which suitable analytical methods can be applied with a view to deduce intelligence relevant to strategy development. Such methods are generic to all industries and need not be dwelled upon here, but comprise chronology lists, source listing, event analysis, alternative scenarios, analysis of competing hypotheses, opportunity analysis and linchpin analysis (Harkleroad and Sawka, 1996). There is a distinct need for future research in the area of CI pertaining to shipping with respect to a survey of existing literature, existing practices, development of new practices, applications and their results in terms of defining strategies and building sustainable competitive advantages.

Having highlighted the relevance to strategy of gathering CI, we can now address some shipping specific environmental factors that CI gathering should encompass and their framing for analytical purposes.

4.3.2.2 Environmental analysis

In practice, a survey of Greek shipping companies’ planning processes indicates a bias towards operating performance, financial projections and functional budgets. Environmental analysis, e.g. PEST (Political, Economic, Social and Technology) analysis, and SWOT (Strengths, Weaknesses, Opportunities and Threats) analysis are considered least important. Of those external elements taken into account, regulatory issues, general business climate and competitive climate score highest, followed closely by technological factors, customer preferences and supplier trends (Koufopoulos et al., 2005).

The observed bias of those shipping companies in approaching planning as a finance-related matter could limit the benefits those companies can obtain from the planning process. This is also suggested by a 2009 McKinsey survey of non-shipping managers who admit to a focus of strategic planning on financial objectives (e.g. cash conservation), yet feel discomforted by the lack viz. absence of an adequate balance between short-and long-term perspectives in their planning process (Cheung et al., 2009). It is noteworthy that Asia-Pacific managers also place financial resources as the second most important constraint on the strategy selection resulting from the strategic reflection process. However, differences in their planning process exhaustiveness did vary by market segment of the shipping company concerned, with liner companies doing more environmental analysis than bulk shipping companies. Similarly, tanker companies seem to do more planning than dry bulk companies (Hawkins and Gray, 2000). The minority who do use specific analytical techniques did so by using the SWOT model (Hawkins and Gray, 2000).

4.3.2.3 Planning formality

The Asia-Pacific shipowners have mostly no formalised strategic plans, but do have a high intensity “discussion process” involving senior management (Hawkins and Gray, 1999). The content of this process is not detailed in the authors’ articles. Asia-Pacific managers seem to pursue strategic objectives regardless of changes in the environment, and as such do not attach much importance to the use of external information, preferring to rely on personal knowledge, experience and intuition. Consequently, a majority see no use for decision support tools such as scenario analysis and simulations (Hawkins and Gray, 1999).

Greek shipping companies, again, do differ in their practice. Their planning formality is mainly geared towards creating a climate supportive of planning efforts and the development of a formal statement. The use of the company’s plans for controlling managerial performance are considered least important as is the acceptance of such plans by the persons who are to attain the goals set out therein (Koufopoulos et al., 2005). This is quite an evolution, as Grammenos and Choi (1999) found Greek shipping companies not to have any formal rules for strategic decision making at all. As such, planning in those shipping companies seems geared towards giving the organisation a sense of direction rather than to develop a detailed plan, (i.e forward looking). The forward-looking nature is also reflected in the perceived emphasis on development of internal capabilities as opposed to backward looking failure analysis (Koufopoulos et al., 2005). Notwithstanding, it is noteworthy that in a historical context Greek shipowners were also noted to have had an “emerging” asset play strategy i.e.