Chapter 8

Dividends and other corporate distributions

ey.com/EYTaxGuide

Most people think they know what dividends are. The problem is that the term is commonly used to describe a large number of items that the IRS does not consider to be dividends. “Dividends” paid by an insurance company to its policyholders are considered by the IRS to be a return of premiums, not dividends. “Dividends” paid by a savings and loan association to its depositors are considered to be interest, not dividends.

So what is a dividend? A dividend is a share of a corporation’s profits that is distributed to shareholders. This chapter discusses how these distributions, as well as other corporate distributions, are taxed.

If you own stock in a company or shares in a mutual fund or real estate investment trust (REIT), you may receive dividend distributions. The distributing company or mutual fund will send you a Form 1099-DIV just after year-end with the total amount of dividends you must report to the IRS on your income tax return. This chapter explains the difference between the various tax forms you may receive and which forms to keep in your records or attach to your income tax return.

This chapter also discusses dividend reinvestment plans (DRPs) that reinvest the dividends in the stock generating them. These plans are provided by companies for all their shareholders and should not be confused with retirement plans run by employers for the benefit of their employees.

Certain dividend income (but not interest income), referred to as “qualified dividend income,” is taxed at a maximum rate of 20% for high income taxpayers who are otherwise in the 39.6% regular income tax bracket (i.e., taxable incomes over $406,750 for individual filers, $432,200 for heads of households, $457,600 married filing jointly, and $228,800 if married filing separately). Qualified dividends received by taxpayers in the 10% and 15% tax brackets are taxed at a zero rate. For all others, the tax rate on qualified is 15%. These preferential tax rates on qualified dividend income apply to both the regular tax and the alternative minimum tax.

Under the Affordable Care Act, the 3.8% Net Investment Income Tax (NIIT) on unearned income—including dividends—took effect for tax years beginning in 2013 and thereafter. For individuals, the tax is 3.8% of the lesser of: (1) “net investment income” or (2) the excess of modified adjusted gross income (MAGI) over $200,000 ($250,000 if married filing jointly or a qualifying widow(er) with dependent child; $125,000 if married filing separately). The NIIT is payable regardless of whether or not you otherwise pay any regular income tax or are subject to alternative minimum tax on your income.

Foreign-source income. If you are a U.S. citizen with dividend income from sources outside the United States (foreign-source income), you must report that income on your tax return unless it is exempt by U.S. law. This is true whether you reside inside or outside the United States and whether or not you receive a Form 1099 from the foreign payer.

This chapter discusses the tax treatment of:

- Ordinary dividends,

- Capital gain distributions,

- Nondividend distributions, and

- Other distributions you may receive from a corporation or a mutual fund.

This chapter also explains how to report dividend income on your tax return.

Dividends are distributions of money, stock, or other property paid to you by a corporation or by a mutual fund. You also may receive dividends through a partnership, an estate, a trust, or an association that is taxed as a corporation. However, some amounts you receive that are called dividends are actually interest income. (See Dividends that are actually interest under Taxable Interest in chapter 7.)

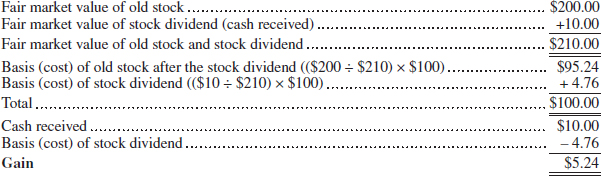

Most distributions are paid in cash (or check). However, distributions can consist of more stock, stock rights, other property, or services.

You may want to see:

514 Foreign Tax Credit for Individuals

514 Foreign Tax Credit for Individuals

550 Investment Income and Expenses

550 Investment Income and Expenses

Schedule B (Form 1040A or 1040) Interest and Ordinary Dividends

Schedule B (Form 1040A or 1040) Interest and Ordinary Dividends

8960 Net Investment Income Tax—Individuals, Estates, and Trusts

8960 Net Investment Income Tax—Individuals, Estates, and Trusts

This section discusses general rules for dividend income.

Tax on unearned income of certain children. Part of a child’s 2014 unearned income may be taxed at the parent’s tax rate. If it is, Form 8615, Tax for Certain Children Who Have Unearned Income, must be completed and attached to the child’s tax return. If not, Form 8615 is not required and the child’s income is taxed at his or her own tax rate.

Some parents can choose to include the child’s interest and dividends on the parent’s return if certain requirements are met. Use Form 8814, Parents’ Election To Report Child’s Interest and Dividends, for this purpose.

For more information about the tax on unearned income of children and the parents’ election, see chapter 32.

Beneficiary of an estate or trust. Dividends and other distributions you receive as a beneficiary of an estate or trust are generally taxable income. You should receive a Schedule K-1 (Form 1041), Beneficiary’s Share of Income, Deductions, Credits, etc., from the fiduciary. Your copy of Schedule K-1 (Form 1041) and its instructions will tell you where to report the income on your Form 1040.

Social security number (SSN) or individual taxpayer identification number (ITIN). You must give your SSN or ITIN to any person required by federal tax law to make a return, statement, or other document that relates to you. This includes payers of dividends. If you do not give your SSN or ITIN to the payer of dividends, you may have to pay a penalty.

For more information on SSNs and ITINs, see Social Security Number (SSN) in chapter 1.

Backup withholding. Your dividend income is generally not subject to regular withholding. However, it may be subject to backup withholding to ensure that income tax is collected on the income. Under backup withholding, the payer of dividends must withhold, as income tax, on the amount you are paid, applying the appropriate withholding rate.

Backup withholding may also be required if the IRS has determined that you underreported your interest or dividend income. For more information, see Backup Withholding in chapter 4.

Stock certificate in two or more names. If two or more persons hold stock as joint tenants, tenants by the entirety, or tenants in common, each person’s share of any dividends from the stock is determined by local law.

Form 1099-DIV. Most corporations and mutual funds use Form 1099-DIV, Dividends and Distributions, to show you the distributions you received from them during the year. Keep this form with your records. You do not have to attach it to your tax return.

Dividends not reported on Form 1099-DIV. Even if you do not receive Form 1099-DIV, you must still report all your taxable dividend income. For example, you may receive distributive shares of dividends from partnerships or S corporations. These dividends are reported to you on Schedule K-1 (Form 1065), Partner’s Share of Income, Deductions, Credits, etc., and Schedule K-1 (Form 1120S), Shareholder’s Share of Income, Deductions, Credits, etc.

Reporting tax withheld. If tax is withheld from your dividend income, the payer must give you a Form 1099-DIV that indicates the amount withheld.

Nominees. If someone receives distributions as a nominee for you, that person should give you a Form 1099-DIV, which will show distributions received on your behalf.

Form 1099-MISC. Certain substitute payments in lieu of dividends or tax-exempt interest received by a broker on your behalf must be reported to you on Form 1099-MISC, Miscellaneous Income, or a similar statement. See Reporting Substitute Payments under Short Sales in chapter 4 of Publication 550 for more information about reporting these payments.

Incorrect amount shown on a Form 1099. If you receive a Form 1099 that shows an incorrect amount (or other incorrect information), you should ask the issuer for a corrected form. The new Form 1099 you receive will be marked “Corrected.”

Dividends on stock sold. If stock is sold, exchanged, or otherwise disposed of after a dividend is declared but before it is paid, the owner of record (usually the payee shown on the dividend check) must include the dividend in income.

Only gold members can continue reading.

Log In or

Register to continue