Consistent treatment of estate items. Beneficiaries must generally treat estate items the same way on their individual income tax returns as they are treated on the estate’s income tax return. For more information, see How and When to Report under Distributions to Beneficiaries From an Estate in Publication 559, Survivors, Executors, and Administrators.

This chapter discusses the tax responsibilities of the person who is in charge of the property (estate) of an individual who has died (decedent). It also covers the following topics:

Filing the decedent’s final return.

Tax effects on survivors.

This chapter does not discuss the requirements for filing an income tax return of an estate (Form 1041). For information on Form 1041, see Income Tax Return of an Estate—Form 1041 in Publication 559. This chapter also does not discuss the requirements for filing an estate tax return (Form 706). For information, see Form 706 and its instructions.

1310 Statement of Person Claiming Refund Due a Deceased Taxpayer

4810 Request for Prompt Assessment Under Internal Revenue Code Section 6501(d)

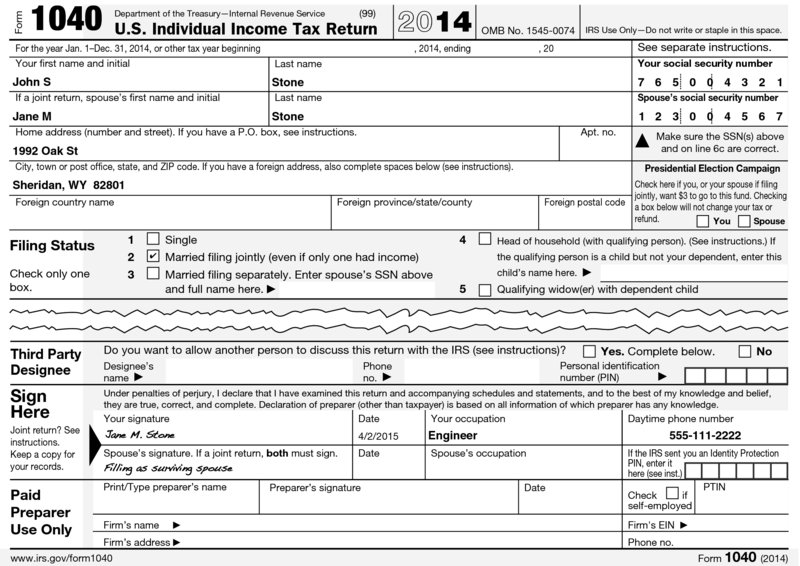

Figure 43-A. Surviving Spouse Filing Joint Return with Decedent

Important Tax-Related Actions to Take After a Death

Action

Comments

Obtain at least 10 death certificates from the local county clerk, mortuary, or funeral director.

The executor or personal representative (referred to as the “executor” in this chart) must file the death certificate with the estate tax return (Form 706) for the decedent. Also, death certificates will be needed to claim life insurance proceeds, change title to bank accounts, and transfer title to other assets. Death certificates usually will not be available until a week or two after the death.

Contact life insurance companies to claim the proceeds. The executor can usually find the telephone number on the most recent life insurance policy statement.

Contact the insurance company as soon as possible. The decedent’s family may need the insurance proceeds for support.

Notify the Social Security Administration of the death. Also notify banks and investment brokers.

The telephone number for the Social Security Administration is 1-800-772-1213.

Contact an estate planning or probate attorney to determine what court filings are necessary.

Select an attorney who has at least 5 years of significant experience handling the administrations of estates. See the attorney as soon as possible after the death. Referrals to attorneys can be obtained from friends or relatives, or often from a local bar association referral service.

Contact an accountant regarding all tax filings that will be necessary.

The personal representative or surviving spouse must file a final income tax return for the decedent (Form 1040). No further estimated taxes for the decedent must be paid after the death of the decedent.

The “probate estate” (if a probate is necessary) becomes a new taxpayer and the personal representative must file a tax return (Form 1041). The estate may select a fiscal year that may result in beneficial tax deferral.

If the decedent funded a “revocable living trust” during life, that trust, which becomes irrevocable at death also becomes a new taxpayer and may also be required to file a Form 1041. However, in certain cases, the probate estate and the trust may file consolidated income tax returns.

Obtain an Employee Identification Number (EIN) for the estate.

The estate will need an EIN to file tax returns and to open a bank account. In addition, the estate will be required to get a new EIN if the funds from the estate are used to establish a trust. The IRS provides an online application with an interactive, interview-style questionnaire that will guide you through the application process. There is no charge to obtain an EIN. The estate’s attorney or accountant can also help with this process.

Open an estate checking account as soon as possible—deposit all checks due to the decedent and pay all debts and expenses owed (including funeral expenses and taxes) from this account.

It is critical to keep accurate records. Do not commingle anyone else’s income or expenses with the decedent’s income and expenses, including income earned and expenses paid after date of death. The executor will need accurate information to file the decedent’s final income tax return, the estate’s and/or trust’s income tax return, and the estate tax return.

Search through the decedent’s desk, office, safe deposit box, and files to locate information that is needed for the tax returns.

Specifically, look for the following: will, codicils to the will and trust agreements; addresses and Social Security numbers of beneficiaries; checking, savings, money market, and CD statements; checkbook registers; brokerage statements; stock certificates; bonds; retirement plan and IRA benefit statements; life insurance and annuity policies; the last 3 years of state and federal income tax returns and all prior gift tax returns; property tax bill and deed for real estate; buy-sell or operating agreements for businesses; all outstanding bills (including last illness and funeral bills); and any undeposited checks.

Review the decedent’s company retirement and benefit plans, as well as IRAs, with a tax advisor or attorney.

The beneficiary of these assets must make certain decisions regarding distributions from these plans and IRAs; the decisions made can have significant income tax consequences.

Only gold members can continue reading. Log In or Register to continue

3 Armed Forces Tax Guide

3 Armed Forces Tax Guide 559 Survivors, Executors, and Administrators

559 Survivors, Executors, and Administrators  56 Notice Concerning Fiduciary Relationship

56 Notice Concerning Fiduciary Relationship 1310 Statement of Person Claiming Refund Due a Deceased Taxpayer

1310 Statement of Person Claiming Refund Due a Deceased Taxpayer 4810 Request for Prompt Assessment Under Internal Revenue Code Section 6501(d)

4810 Request for Prompt Assessment Under Internal Revenue Code Section 6501(d)