Climate change and the construction industry: sustainability challenges for Singapore

Climate change and the construction industry: sustainability challenges for Singapore

12.1 Introduction

There is overwhelming scientific consensus that since pre-industrial times increasing emissions of greenhouse gases (GHGs)1 have led to a marked increase in atmospheric GHG concentrations (IPCC, 2007), causing global warming. The causes for this phenomenon, more popularly known as climate change, can be divided into two categories, namely, natural causes and those that are created by man. The natural factors responsible for climate change include the continental drift, volcanoes, ocean currents, the earth’s tilt, and comets and meteorites. The human factors include industrial wastage, use of natural resources for human consumption and habitation, population increase and the extreme reliance on the use of fossil fuels and natural gases.

Of the human-induced causes of climate change, it is said that the energy sector is responsible for about three-quarters of the carbon dioxide (CO2) emissions in the world (IPCC, 2001). The construction industry is said to be not too far behind, as it is one of the most energy intensive industries. According to the American Institute of Architects (AIA, 2000), the biggest source of emissions and energy consumption both in the U.S. and around the globe is said to be the construction industry and the energy it consumes each year. According to a briefing note prepared for the International Investors Group on Climate Change (Kruse, 2004), the cement sector alone is said to account for 5 percent of global man-made CO2 emissions. Further, mining and manufacturing of raw materials used in construction and the transportation of heavy building materials are said to be contributing significantly to climate change.

In heavily urbanized Singapore, where half the total land area is built up, the construction sector is said to account for approximately 16 percent of national emissions of CO2 (MEWR, 2008). This figure, however, includes emissions resulting from primary and secondary energy consumption by buildings and excludes the emissions from the industrial process involved in the construction industry. Hence, the total of direct and indirect emissions resulting from the construction industry could be much higher.

In the circumstances, it is not difficult to argue that the construction industry is one of the major industries responsible for high levels of GHG emissions, which cause climate change. Thus, in many jurisdictions, the construction sector has been identified as one of the key industries that should be pro-active in engaging in sustainable development by curtailing the GHG emissions and adopting more sustainable energy consumption patterns.

It should also be pointed out that, in addition to being energy efficient and helping mitigate climate change, the construction industry has another role to play in sustainable development. That is, improving the capacity to adapt to changing climate conditions and the related risks. For example, weatherrelated impacts such as hurricanes, flooding, and coastal erosion for which climate change is at least partially responsible, would require the use of new building techniques and materials to withstand adverse weather conditions. Such events would also influence the choice of site for construction projects.

Some authors (Mimura et al., 1998) note that cost increases for disaster rehabilitation and countermeasures against natural calamities caused by climate change could expand the market for the construction industry. However, the flip side is that flooding and other extreme weather-related events mentioned above could damage buildings and infrastructure and cost countries billions of dollars in repair and reconstruction work. This would require diversion of precious funds earmarked for other development activities. Thus, whilst the GHG emissions by the construction industry are one of the major causes for climate change, the construction industry could also be one of the worst affected industries due to impacts of climate change.

Due to its geographic location, South East Asia has been identified as one of the most vulnerable regions to environmental risks associated with climate change. Further, the rising sea levels and the consequent flooding from the sea may also adversely affect the coastal areas in this region (IPCC, 2007). In the circumstances, it is important that the countries in the South East Asian region identify the climate change-related environmental risks to the construction industry and take initiatives to mitigate such risks.

Being a small island city state off the southern tip of the Malay Peninsula, with only 710.2 km2 of land, Singapore is the smallest nation in South East Asia. However, with approximately 5 million people living in the small island, including approximately 2 million foreign workers, Singapore can be considered a densely populated, compact, cosmopolitan city. With its population expected to grow to 6 million by 2020, the construction sector in Singapore is expected to boom. Thus, the introduction of energy-efficient technologies and environmentally friendly designs and construction methods as measures to mitigate climate change whilst trying to keep the construction cost affordable to the end-users, will be one of the biggest challenges Singapore will face in the coming years. Singapore will be one of the countries in South East Asia constantly under threat due to sea erosion and rising sea levels. Thus, in addition to taking measures to reduce the GHG emissions from the construction sector, another challenge for Singapore will be to improve the adaptability of its construction industry to climate change.

12.2 Dealing with climate change and the impact on the construction industry

12.2.1 Kyoto Protocol

According to the United Nations Environmental Programme (UNEP), currently over 200 international environmental agreements and a large number of bilateral agreements on the subject of environment exist. However, the Kyoto Protocol, a protocol to the United Nations Framework Convention on Climate Change (UNFCCC)2 which was agreed on 11 December 1997, is the only multilateral framework we have to address climate change.

The Kyoto Protocol establishes emission reduction targets for the period 2008–2012 for the industrialized countries (Annex 1 countries).3 As far as developing countries are concerned, there are no reduction targets. However, developing countries are encouraged under the clean development mechanism (CDM),4 one of the three mechanisms introduced to deal with global climate change,5 to benefit from transfer of technology, and foreign investments flows into sectors such as renewable energy and afforestation projects which would contribute to mitigate GHG emissions. However, this mechanism appears ineffective as it does not monitor fair distribution of CDM projects among the developing countries (Gunawansa, 2009).

The Kyoto Protocol could be criticized for having only a limited life span and also for having binding obligations only upon the Annex 1 countries. Further, as far as adaptation is concerned, the Kyoto Protocol has not established any effective mechanism, although it requires countries to formulate, implement, publish and regularly update, national and, where appropriate, regional programmes containing measures to mitigate climate change and measures to facilitate adequate adaptation to climate change.6 Further, although, the Kyoto Protocol has established an adaptation fund to finance concrete adaptation projects and programmes in developing countries,7 it is ineffective, as it does not have specifically quantitative funding commitments for the countries.

The Kyoto Protocol does not contain any specific provisions directly impacting on the construction industry. However, it is likely that various legislative and policy instruments the Annex I countries introduce to meet their mandatory GHG reduction targets during the period 2008–2012, and the self-induced initiatives that non-Annex 1 countries might take to reduce the emission of GHGs, might have a direct or indirect impact on the construction industry in their individual jurisdictions, as it is one of the most energy-intensive industries.

12.2.2 National initiatives

Despite the lack of effective multilateral consensus on the responsibility of each state to deal with climate change, since the Earth Summit in 1992,8 several nations of the world have been working towards reducing the emission of GHGs at the national level. The examples given below from the U.S., Australia and Singapore prove this point. Some of these initiatives take the form of specific legislation aimed at imposing penalties and taxation to force people and industries to adapt climate-friendly behavioural patterns and to promote sustainable development. There are other policy initiatives without specific legislation to back them. There are also voluntary industrial standards that have been introduced.

It is important to note that although the U.S. has so far not agreed to meet any mandatory GHG reduction targets under the Kyoto Protocol, 28 U.S. states have programmes to curb CO2 emissions and at least 166 U.S. cities have agreed to apply the Kyoto emission reduction standards to their communities (Prato and Fagre, 2006). For example, in August 2006, the California State Legislature passed the Global Warming Solutions Act (AB32) which is designed to reduce the State’s impact on global warming. AB32 requires a reduction of statewide GHG emissions to 1990 levels, roughly a 25 percent reduction under business-as-usual estimates, by the year 2020, using a mandatory statewide cap on emissions beginning in 2012.

The state of Wisconsin has mandated a 30 percent improvement in the energy efficiency of state buildings.9 Some other initiatives are under consideration. One such initiative concerns the proposal for the adoption of the International Energy Conservation Code (IECC) for commercial buildings, which is projected to increase the energy efficiency of new buildings by 30 percent. It is said that the overall objective of these measures targeting buildings is to achieve zero energy usage for new residential and commercial buildings by 2030.10

Other states too have since followed suit, passing similar legislation. For example, the states of Oregon, New Jersey and Hawaii passed legislation in 2007 that imposed mandatory caps on GHG emissions. In Florida, the Governor has signed three executive orders in July of 2007 that set GHG emissions reduction targets for the State (PEW Centre, 2007). These instruments will have a definite impact on the construction industry due to the high energy-intensive nature of the sector.

Australia ratified the Kyoto Protocol only in December 2007. Thus, any efforts taken by Australia to formally meet its obligations under the Kyoto Protocol are still at an infant stage. According to Australia’s Department of Climate Change, the country has set a long-term target for national emissions reductions of 60 per cent on 2000 levels by 2050. The building and construction sector is a key focus area for Australia’s climate change response. This is because the energy use in the commercial building sector is said to generate almost 10 percent of Australia’s GHG emissions according to a baseline study carried out by the Australian Greenhouse Office (Australian Greenhouse Office, 2005). The same source suggests that emissions could double between 1990 and 2010.

There are numerous environment rating schemes for buildings across Australia, that have been developed by local, state and federal governments, even though specific legislation is yet to be introduced. National Australian Built Environment Rating System (NABERS) is one example of a voluntary environmental rating system for office premises that has been developed by the Australian government. It is aimed at existing buildings and covers a range of environmental issues such as GHGs, water, stormwater, transport, landscape diversity, waste and toxic materials. It measures actual performance against set benchmarks.11 It is tailored for use by building owners, managers and building occupants. Building owners and managers will be able to report on those aspects of the environmental performance of the building that are in their control, for example landlord energy use (lifts, air conditioning etc.) and water consumption. Building occupants will report on the environmental performance of the aspects of the building that they control (light and power in their tenancy, transport to and from the building etc.).

The Australian Building Greenhouse Rating Scheme (ABGRS), which rates the GHG performance of new and existing office buildings against benchmarks is another example. Separate ratings can apply to tenancies, core buildings or whole buildings. Actual performance must be demonstrated once the building is operating. The scheme requires buildings to report their actual annual energy use and GHG emissions, and buildings (and/or their tenancies) can only keep their ABGR star ratings if they continue to meet their target consumption levels. The rating system allows the developers, owners and occupants of office buildings to rate their greenhouse performance on a simple scale of one to five stars. Buildings that perform better receive more stars. A good rating can be a significant advantage in the commercial property market. ABGRS is now a part of NABERS and is known as NABERS Energy.12

Another example from Australia is the ‘Green Star’ rating system developed by the Green Building Council of Australia (GBCA). It is a national environmental rating tool for buildings which rates a building in relation to its management, the health and wellbeing of its occupants, accessibility to public transport, water use, energy consumption, the embodied energy of its materials, land use and pollution. Green Star aims to assist the building industry in its transition to sustainable development.13

In Singapore, the Green Mark Scheme introduced by the government, which will be discussed in more detail later, has introduced a mandatory certification system for buildings to establish national sustainability requirements in the construction sector.

12.3 The case of Singapore

12.3.1 Key sustainable development challenges

As noted in the introduction, Singapore is a small island city-state with limited land space. However, although it is the smallest nation in South East Asia, in terms of gross domestic product (GDP) purchasing power parity (PPP) per capita,14 it is currently considered as the fifth wealthiest country in the world according to the International Monetary Fund (IMF)15 and the eighth wealthiest according to the U.S. Central Intelligence Agency’s World Fact Book for 2009.16 According to the government statistics, as of January 2010, Singapore’s official reserves stood at US$189.6 billion.17 Thus from an economic point of view, Singapore may not face sustainable development challenges faced by developing countries in the region.

According to Singapore’s Minister for National Development Mah Bow Tan, ‘We want to develop without squandering resources and causing unnecessary waste. We want to develop without polluting our environment. We want to develop, while preserving greenery, waterways, and our natural heritage’ (Gov Monitor, 2010b). Thus Singapore’s overall goal seems to be to grow in an efficient, clean, and green way. One of the biggest development challenges Singapore will face in achieving this is its lack of natural resources, having to rely on other countries and foreign trade for resources such as water,18 fuel and food. Malaysia is presently supplying around 40 percent of Singapore’s water needs. With approximately 2,440,000 barrels of oil imported per day, Singapore is currently ranked the seventh largest importer of oil.19

The country’s average wind speeds are considered to be too low for the economical use of large wind turbines. The use of wave, tidal and ocean thermal resources have been ruled out due to their limited application and as the available sea space is used for ports, anchorage and shipping lanes. Singapore’s geography also does not present opportunities to harness renewable energy from hydro or geothermal technologies (MEWR, 2008). Thus, the island will have to focus on raising efficiency of the current energy usage. At the same time, research and development of alternative energy sources will have to be financed.

Likewise, given Singapore’s lack of water resources and the current reliance on imported water for consumption, the country will have to take initiatives to use water more conservatively by reducing the current level of consumption. Such initiatives will have to be supported with investment in infrastructure for waste water recycling and desalination of sea water.

Another key challenge is that, with no natural hinterland, Singapore has to accommodate homes, offices, industrial premises, infrastructure for utilities, parks, roads, reservoirs, airport, military facilities and many others within its small land area, whilst ensuring that a clean, green and comfortable environment to live in is provided for the people. The answer, as far as the building and construction sector is concerned, is the development of high-rise public housing, office complexes and administrative buildings in small spaces. This would, however, lead to congested and environmentally unsustainable conditions if adequate measures are not taken to develop sustainable living and working environments.

12.3.2 Construction sector in Singapore

Except for the ripple effect of the current global economic recession, it could be said that Singapore has experienced a construction boom during the last two decades, having gone through a lean period during the 1997 Asian financial crisis, followed by the terrorism threat in the region and the SARS outbreak (Chan and Gunawansa, 2008). As a result, construction is taking place in all sectors of the economy. Projects range from domestic housing and office towers through to sophisticated infrastructure developments and construction of massive resorts, hotels and other tourist attractions.

According to the Singapore government, the construction experts of BIS Shrapnel have claimed that, of the countries in Southeast Asia, the boom market will mostly benefit countries such as Singapore and Vietnam due to the rising activity in each of their domestic residential building sectors (EBIS, 2007). The rising property prices in Singapore serve as a proxy of investors’ confidence in the business conditions in Singapore.

According to the Government of Singapore, in 2009, the construction sector enjoyed strong double-digit growth for the third consecutive year, driven by exceptionally strong construction demand in the preceding two years (Gov Monitor, 2010a). As a result, the industry achieved a record level of on-site construction activity or output of about $30 billion. However, the global financial crisis had a considerable impact on the construction industry in 2009, especially on private sector demand. This is evidenced by the drop in the value of contracts awarded in 2009 to $21 billion from a record high of $35.7 billion in 2008. Out of this 64 percent were public sector contracts which establish the need for public sector housing and other infrastructure facilities to cater for the growing population.

In the circumstances, a major challenge in connection with the construction sector would be the need to balance the growth of the industry with the need to mitigate the emission of GHGs and improve the adaptive capacity of buildings and infrastructure facilities to adverse impacts of climate change.

12.3.3 Commitment to reduce GHG emissions

Having ratified the Kyoto Protocol in April 2006, Singapore has made a voluntary commitment to reduce its carbon intensity by 25 percent from 1990 levels by the year 2012, although it does not have to meet any mandatory GHG reduction targets during the first commitment period. According to the Singapore Ministry of Environment and Water Resources (MEWR), in fact, the country had achieved a 22 percent reduction in 2004 (MEWR, 2006). Further, according to figures from the National Environment Agency (NEA), Singapore’s carbon intensity was at 0.28 kilotonnes per SGD million in 1990 (NEA, 2002). That figure has declined to 0.21 in 2005, representing a 25 percent reduction. Thus, it could be said that Singapore is well on track to meet its reduction goals by 2012.

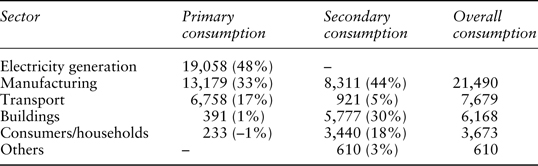

According to MEWR, the main contribution to Singapore’s GHG emissions is CO2. Table 12.1 shows CO2 emissions in Singapore from the five key sectors, namely, power generation, manufacturing, transport, buildings and households, in terms of both primary and secondary consumption in 2004 (primary users are those that combust fuel directly while secondary users are those that use the electricity generated from fuel).

Table 12.1 Key CO2 contributors in 2005

Source: Adapted from MEWR, 2006.

A clear indication from the Table 12.1 is that when the primary and secondary usage is put together, the building sector is one of the main contributors to GHG emissions in Singapore.

12.4 Singapore’s framework for environmental management

Until the late 1990s, the laws on environment that existed in Singapore were diverse and scattered throughout many Acts. Further, state agencies in charge of environment-related subjects were many. However, this problem has been resolved to a considerable extent with the enactment of two key statutes, namely, the Environmental Public Health Act (EPHA),20 which controls waste including toxic, domestic and industrial waste, and the Environmental Protection and Management Act (EPMA)21 which consolidated various laws including the Clean Air Act and the Water Pollution Control and Drainage Act. It applies to air, water, noise, land contamination and hazardous substances.

In 2002, Singapore established the National Environmental Agency (NEA).22 NEA’s powers include inter alia:

prescribe and implement regulatory policies, strategies, measures, standards or any other requirements on any matter related to or connected with environmental health, environmental protection, radiation control, resource conservation, waste minimization, waste recycling, waste collection and disposal and such other subject matter as may be necessary for the performance of the functions of the Agency.23

Today, Singapore’s framework for environmental management is based on five fundamental principles, namely, control of pollution at source; preemption and taking of early action; the “polluter pays” principle; innovation and new technology; and environmental ownership. According to Singapore’s Ministry of Environment and Water Resources (MEWR) its mission is to ‘to deliver and sustain a clean and healthy environment and water resources for all in Singapore.’24