For 2014, there are two tax credits available to persons who pay expenses for higher (postsecondary) education. They are:

The American opportunity credit, and

The lifetime learning credit.

The chapter will present an overview of these education credits. To get the detailed information you will need to claim either of the credits, and for examples illustrating that information, see chapters 2 and 3 of Publication 970.

Can you claim more than one education credit this year? For each student, you can choose for any year only one of the credits. For example, if you choose to take the American opportunity credit for a child on your 2014 tax return, you cannot, for that same child, also claim the lifetime learning credit for 2014.

If you are eligible to claim the American opportunity credit and you are also eligible to claim the lifetime learning credit for the same student in the same year, you can choose to claim either credit, but not both.

If you pay qualified education expenses for more than one student in the same year, you can choose to take the American opportunity and the lifetime learning credits on a per-student, per-year basis. This means that, for example, you can claim the American opportunity credit for one student and the lifetime learning credit for another student in the same year.

Differences between the American opportunity and lifetime learning credits. There are several differences between these two credits. These differences are summarized in Table 36-1, later.

Caution. You can claim both the American opportunity credit and the lifetime learning credit on the same return—but not for the same student.

American Opportunity Credit

Lifetime Learning Credit

Maximum credit

Up to $2,500 credit per eligible student

Up to $2,000 credit per return

Limit on modified adjusted gross income (MAGI)

$180,000 if married filing jointly; $90,000 if single, head of household, or qualifying widow(er)

$128,000 if married filing jointly; $64,000 if single, head of household, or qualifying widow(er)

Refundable or nonrefundable

40% of credit may be refundable

Credit limited to the amount of tax you must pay on your taxable income

Number of years of postsecondary education

Available ONLY if the student had not completed the first 4 years of postsecondary education before 2014

Available for all years of postsecondary education and for courses to acquire or improve job skills

Number of tax years credit available

Available ONLY for 4 tax years per eligible student (including any year(s) the Hope credit was claimed)

Available for an unlimited number of years

Type of program required

Student must be pursuing a program leading to a degree or other recognized education credential

Student does not need to be pursuing a program leading to a degree or other recognized education credential

Number of courses

Student must be enrolled at least half time for at least one academic period beginning during the tax year

Available for one or more courses

Felony drug conviction

At the end of 2014, the student had not been convicted of a felony for possessing or distributing a controlled substance

Felony drug convictions do not make the student ineligible

Qualified expenses

Tuition, required enrollment fees, and course materials that the student needs for a course of study whether or not the materials are bought at the educational institution as a condition of enrollment or attendance

Tuition and fees required for enrollment or attendance (including amounts required to be paid to the institution for course-related books, supplies, and equipment)

Payments for academic periods

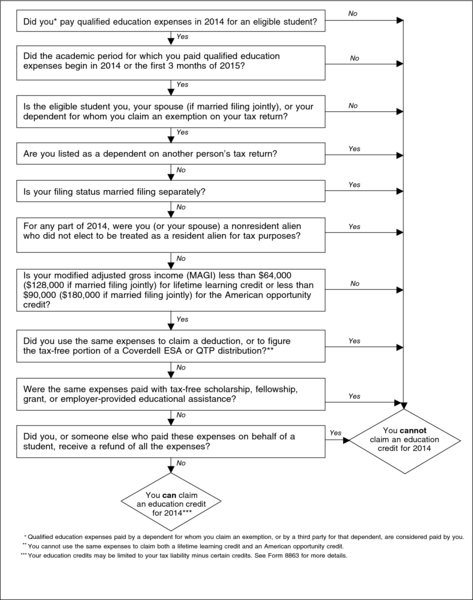

Payments made in 2014 for academic periods beginning in 2014 or beginning in the first 3 months of 2015

You may be able to claim an education credit if you, your spouse, or a dependent you claim on your tax return was a student enrolled at or attending an eligible educational institution. The credits are based on the amount of qualified education expenses paid for the student in 2014 for academic periods beginning in 2014 and in the first 3 months of 2015.

For example, if you paid $1,500 in December 2014 for qualified tuition for the spring 2015 semester beginning in January 2015, you may be able to use that $1,500 in figuring your 2014 education credit(s).

Academic period. An academic period includes a semester, trimester, quarter, or other period of study (such as a summer school session) as reasonably determined by an educational institution. In the case of an educational institution that uses credit hours or clock hours and does not have academic terms, each payment period can be treated as an academic period.

Eligible educational institution. An eligible educational institution is any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education. It includes virtually all accredited public, nonprofit, and proprietary (privately owned profit-making) postsecondary institutions. The educational institution should be able to tell you if it is an eligible educational institution.

Certain educational institutions located outside the United States also participate in the U.S. Department of Education’s Federal Student Aid (FSA) programs.

Who can claim a dependent’s expenses. If an exemption is allowed as a deduction for any person who claims the student as a dependent, all qualified education expenses of the student are treated as having been paid by that person. Therefore, only that person can claim an education credit for the student. If a student is not claimed as a dependent on another person’s tax return, only the student can claim a credit.

Expenses paid by a third party.

Only gold members can continue reading. Log In or Register to continue

970 Tax Benefits for Education

970 Tax Benefits for Education  8863 Education Credits (American Opportunity and Lifetime Learning Credits)

8863 Education Credits (American Opportunity and Lifetime Learning Credits)